Royal Unibrew

Royal Unibrew is an interesting Beverages company listed on the Copenhagen Nasdaq exchange under the ticker RBREW. It has ~49.4mm outstanding shares, trading at DKK676.60, with a market cap of DKK33.5bn. Adding on net debt of DKK1.8bn and minority interest of DKK31mm, Royal Unibrew has an enterprise value (EV) of DKK35.4bn.

Image Source: Company website

RBREW is a regional multi-beverage provider that serves primarily Finland, the Baltic States, Denmark, Germany, Italy, France, and selected international markets. Non-alcoholic beverages make up 49% of net revenue, beer makes up 35%, and other alcoholic beverages 16%. The company produces, markets, sells and distributes mainly their local/regional branded products, and also offer license based international brands of PepsiCo and Heineken in Northern Europe.

The company first caught my attention as a business that has been coping well during COVID19 despite being in an industry that has been quite badly hit. If you look at other Beverages companies like Coca-Cola, Heineken, and Pernod Ricard, most of their operations have been severely affected by the pandemic, as the boost in off-trade sales is not sufficient to cover for the decrease in on-trade sales. As countries went into lockdowns, most of these companies lost close to 100% of their on-trade businesses in late March and early April. Typically, these on-trade businesses also have higher margins. Volumes, product mix and sales took a big hit, and operating deleverage kicked-in, which led to a decrease in Operating Profit margin, and a bigger hit to Operating Profits.

Contrast to RBREW, which executed very well amidst the pandemic. Despite a 10% drop in topline in 2Q20, the company managed to increase its Earnings Before Interest and Taxes (EBIT) Margin by 60bps! Discretionary spending was cut quickly, shifts were adjusted according to demand (allocate resources from on-trade to off-trade), more frequent re-planning of production etc. led to strong cost management. Furthermore, the company increased its focus on free cash flow generation and optimized its working capital, leading to only a 3.6% decrease in free cash flow as compared to 1H2019. As we move out of the lockdowns in 3Q20, results were even stronger - organic revenue growth of 6%, lower cost of production and SG&A expenses led to an EBIT growth of 22% as compared to 2019! Consequently, despite the difficult Q2, Q1-Q3 total net revenue is down ~1%, EBIT is up 5%, and the company is tracking to a full year EBIT of DKK1.5bn, an increase of ~2% yoy. Dividends per share of DKK12.20 (~DKK600mm) was paid in the third quarter, and RBREW also reinitiated its share buyback program, targeting DKK445mm for 2020, which will lead to ~DKK1,045mm of returns back to the equity holders.

Strong execution

Speaking of execution, this company has been executing very well over the last few years. The management is well aware that consumer trends are changing in the beverages space, and that they have to adapt or risk being left behind. Consumers are increasingly demanding beverages that are healthier (low/no sugar/carbs) and more authentic (craft alcohol/local roots), and are also more concerned about sustainability. RBREW has been strengthening and investing into such trends through both organic innovation and also strategic acquisitions (more on this later).

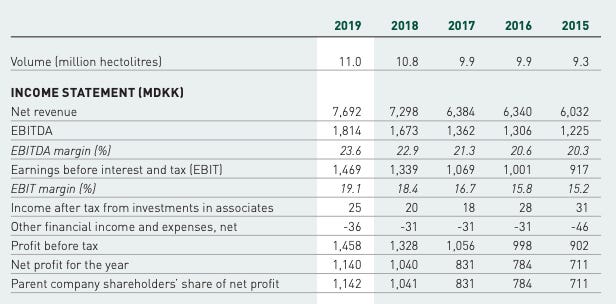

Despite structural headwinds in the industry (higher exise taxes, increased regulation etc.), from 2015-2019, the company has been growing volume at 4.3%, net revenue at 6.3%, and EBIT at 12.5%. EBIT margin expanded from 15.2% to 19.1% over four years!

Image Source: Royal Unibrew 2019 Annual Report

The company is also a cash flow generating machine. Cash conversion has consistently remained close to 100% (2019 at 102%), and the company has been returning most of its cash back to shareholders in the form of dividends (40-60% payout ratio) and share repurchases, at the same time targeting a net debt/EBTIDA ratio of 2.5x, and equity ratio of more >30%. The company has been able to maintain negative net working capital consistently, which effectively means that the company has been able to fund its growth by borrowing from its suppliers. Negative net working capital typically arises when a business is able to sell its products and receive the cash from its customers before it needs to pay its suppliers.

As I combed through the annual reports since 2013, I quickly realised that organic growth is nowhere as high as reported growth, and that a significant part of the growth strategy is through inorganic growth, i.e., acquisitions. RBREW has had a very good track record of buying and more importantly, integrating its acquistions. Buy a company that fits into the overall strategy, integrate the operations, achieve cost synergies, streamline operations, rejuvenate the acquired brands, and increase the operating margins of the acquired company. Rinse and repeat.

Another lever for EBIT growth has been the expansion of EBIT margin. As mentioned above, EBIT margin has been steadily increasing since 2013 (the furthest back I went, also in part to learn more about the Hartwall acquisition), from 12.5% in 2013 to 19.1% in 2019. Furthermore, for the first three quarters of 2020, in the midst of a once in a generation pandemic, EBIT margin for Q1-Q3 2020 was at 21.7%, and is on track for further expansion this year!

The strategy thus far seems to be:

Organic growth + acquisitions + EBIT margin expansion, leading to

Low-mid teens EBIT growth + dividends + share repurchases, leading to

Mid teens diluted EPS growth

Underpinning the above strategy is the high returns of capital and high cash conversion ratio of the company.

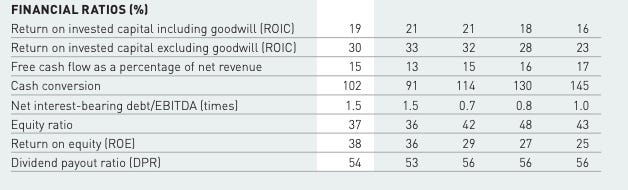

Image Source: Royal Unibrew 2019 Annual Report

Return on invested capital (ROIC) has been high. The company usually includes two ROIC numbers, including and excluding goodwill, and seems to emphasize its ROIC excluding goodwill, which is the higher number. However, I will place more emphasis on the ROIC number including goodwill, as I believe acuiqisitons has been and will continue to be key to the growth of the company. Therefore it is essential to include goodwill in the invested capital. ROIC including goowill has been around the 20% level, which is high compared to the general market and also the industry.

Currently, RBREW returns most of its cash back to its shareholders through a combination of dividends and buybacks, and when there are little/no acquisitions, the excess cash will be used to pay down debt. However, once the company identifies an acqusition, they will use any excess cash they have, and lever up again to finance the acquisition. The high ROIC, coupled with its cash flow generating capabilities, enables the company to maintain a high payout ratio to its shareholders, while at the same time continue to grow its revenue and EBIT (mainly through acquisitions).

So what does this mean for me?

The Beverages industry is facing a few structural headwinds, such as the general shift away from beer/soda to healthier drinks. RBREW has been trying to proactively shift its portfolio to ride on these trends, which has resulted in low-single digit organic growth through the years. There are a few key questions:

1) Can the company continue to expand its EBIT margin, which is now at the high end of its industry at ~21%? New acquisitions will likely be dilutive to margins, at least in the first few years. The current EBIT margin is probably higher than normalized levels due to decreased marketing spending this year

2) Can the company continue to acquire and integrate well? With organic growth at low single-digits, acquisitions will continue to be a key part of the investment thesis. The ability to acquire and integrate well will determine if the company is able to maintain its high ROIC and free cash flow conversion ability. The new CEO has been with the company for 25 years, and has served as a member of the Executive Board since 2011, first as CFO and most recently as COO. It is reasonable to expect the company to continue with its acquisition strategy for the next few years

3) RBREW is currently trading at EV/2019 sales of 4.6x and EV/2019 EBIT of 24x. These ratios are in the higher range of the Beverages industry. Assuming the company continues to grow topline at ~7% (organic + acquisitions), and is unable to expand its EBIT margin further (maintaining at ~21%), and adding on shareholder returns of 3%, total shareholder return should be ~10% p.a. for the next few years

There are a few other considerations to this. On the one hand, net debt to EBITDA is currently quite low as compared to its target level and historical levels, and the company has the capacity to buy back more shares to improve shareholder returns. On the other hand, the above calculation assumes no change in multiple - if you model in a multiple fade over the next few years, total returns will be lower.

Conclusion

All in all, RBREW has been executing well in a difficult industry, and spits out large amount of free cash flow every year. The company has been growing sales both organically and inorganically through product innovation and acquisitions, with substantial improvement in EBIT margin via product mix and operational leverage. This has led to low teens EBIT growth over the last few years, and when coupled with substantial share buybacks, a more than doubling of diluted earnings per share (EPS) from 2014-2019 (mid-teens CAGR). Future returns would likely be lower as EBIT margin has little room left for improvement. Given its successful acquisition and integration track record since 2014, a 10% p.a. total shareholder return for the next few years is a plausible outcome in my opinion.