Boston Scientific Corp

Looking past the TAVR setbacks

Disclaimer: This is not investment advice. I am merely detailing and documenting my investment and thought process. Please do your own due diligence before investing.

I currently have a long position in Boston Scientific Corp shares.

Company description

Boston Scientific Corp (Ticker: BSX) is a global manufacturer and provider of medical devices and equipment used in a broad range of interventional medical specialties. The company has been focusing on minimally-invasive medicine, providing alternatives to surgery and other medical procedures that might be traumatic to the body.

Source: Company presentation in JP Morgan Health Conference January 2020

As mentioned above, I have a moderate long position in Boston Scientific Corp (“BSX”) in my portfolio. I will detail below several key highlights of the narrative, and my thought process in this investment. The article will be broadly divided sequentially into:

Addressing the recent setbacks in TAVR

Portfolio and pipeline highlights

Management team and recent acquisitions

Financials and numbers

Key risks

Addressing the elephant in the room - recent setbacks in TAVR

Transcatheter Aortic Valve Replacement (“TAVR”) has been one of the most exciting and fastest-growing category in the Medical Devices industry. This has also been one of the focus areas for BSX, given its strong growth, and also BSX’s historical leadership in the cardiovascular segment.

The company’s share price has de-rated significantly recently on the back of a couple of setbacks in the TAVR space - down ~20% from mid-October 2020.

Source: https://www.mayoclinic.org/tests-procedures/transcatheter-aortic-valve-replacement/about/pac-20384698

TAVR Background

TAVR is a minimally invasive procedure to replace a narrowed aortic valve in patients with severe aortic stenosis. The doctor will insert a catheter in your leg or chest and guide it to the patient’s heart to replace the old valve with a new valve. This is less invasive and doesn’t need to open up the patient’s chest (as opposed to SAVR), which exposes the patient to other side effects and risks.

BSX had been attacking this market with a dual-valve strategy. Lotus Edge, a more niche valve used for a smaller segment of high-risk patients, and Acurate neo, which is more of a “workhorse” valve that can be used for a larger segment of patients. Lotus Edge was just approved in the US for high-risk patients, and Acurate neo has been availabe in Europe for a while, and is also in the midst of launching its next generation platform Acurate neo2 in Europe.

The launch of Lotus Edge in the US was supposed to be one of the key growth drivers for the company in the next few years. Management also expected Acurate neo to be approved in the US in 2021, mainly based on SCOPE I and II clinical trial data. Therefore, the original expectation was to have two differentiated valves in the US by 2021 to help gain share in this $5bn market, which has been dominated by Medtronic (“MDT”) and Edward Lifesciences (“EW”).

What happened?

First, during its TCT update in Oct 2020, BSX announced that Acurate neo failed its primary endpoint in SCOPE II trial, a head-to-head against Medtronic’s CoreValve Evolut. As such, BSX no longer plans to use data from SCOPE I and SCOPE II in its filing for Acurate Neo2 FDA approval, and now projects potential Food and Drug Administration (“FDA”) approval in 2024, as compared to its previous projection of 2021. At the same time, management also pushed back Lotus Edge’s entry into the intermediate-risk segment, due to slower enrollment in the REPRISE IV intermediate-risk trial, from 2022 to 2024. As a result, the stock price fell 4% on a day of flat trading for the broader market.

The next whammy came around one month later, when BSX announced a complete withdrawal of the Lotus Edge system globally. This was unexpected, to say the least, and the timing could not have been worst coming so close after the TCT update. This raised questions among investors, and also shook their confidence in the management team. The stock price fell 8% on the day and continued to fall since.

The main reason cited for the withdrawal is the complexity and cost related to deliver and support Lotus Edge in the field, especially given its more niche market. Weighing against the other high-growth options that BSX currently has, the management made the tough decision to withdraw the Lotus platform, and focus the company’s time and resources on other parts of the portfolio.

So what?

TAVR continues to be dominated by MDT and EW, even more so now as BSX withdraws its Lotus Edge system. Both MDT and EW’s valves have been approved by FDA for low-risk patients, which vastly expanded their addressable market.

I believe the main reason why the share price dropped so much over these couple of months is not that there will be a huge financial impact on the company. Yes, Lotus is an important growth driver. Yes, BSX will not have a TAVR valve in the US market for the next 3 years. Yes, revenue and earnings estimates have come down slightly (1-2% on the topline, lesser on the bottom line) over the next few years.

But I think that the main issue here is more of confidence and sentiment. This revision to the financials does not warrant a 20% drop in share price. Rather, investors worry about “what’s next”? As Warren Buffett famously said in one of his annual letters to shareholders:

“In the world of business, bad news often surfaces serially: you see a cockroach in your kitchen; as the days go by, you meet his relatives,”

My take is that even though this is a disappointing turn of events, I believe that discontinuing the Lotus platform is the right choice given the complexity and associated costs in Lotus, and also the competitive landscape. It makes sense to cut loss, move on, and prioritize other high growth areas in the overall portfolio. Which brings me to my second key point below.

BSX has a premium Medical Devices portfolio that has grown and will probably continue to grow above market in the medium term.

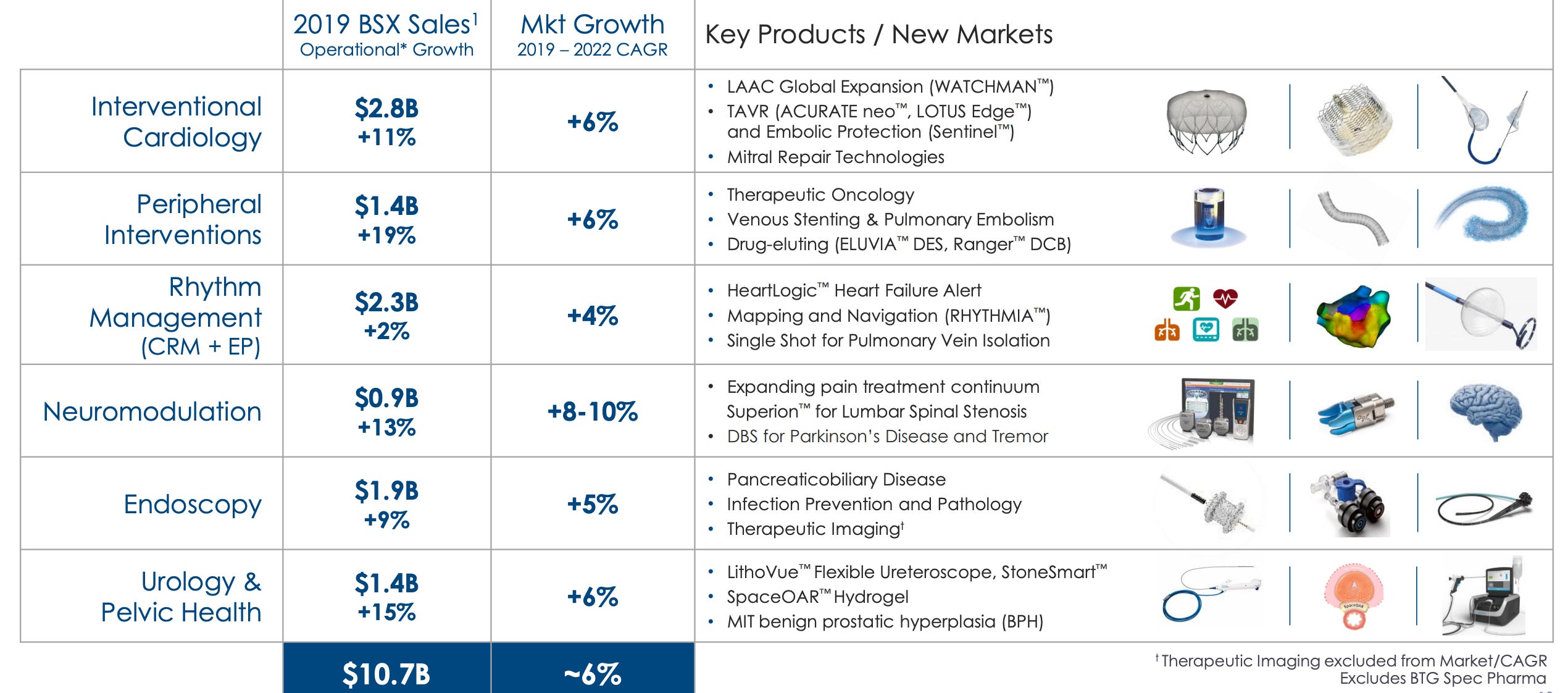

BSX’s recent launches and it’s pipeline over the next few years is one of the most attractive in the medical devices space, and is a key part to the investment thesis. There are several exciting growth opportunities across its entire portfolio, including Watchman, Sentinel, and Acurate neo2 (EU) in Structural Heart, Exalt D and Exalt B in Endoscopy, SpaceOAR, Rezum, and LithoVue in Urology, Interventional Oncology, Eluvia and Ranger (especially after the Paclitaxel issue in 2019) in Peripheral Interventions, and WaveWriter and Vertiflex in Neuromodulation.

Source: Company Investor Presentation. Note that Lotus is still here as this is a Jan 2020 presentation

I will highlight below two of the most exciting - Watchman and single-use scopes.

Watchman

The majority of BSX’s Structural Heart revenues currently comes from Watchman. Watchman is a Left Atrial Appendage Closure (“LAAC”) device that utilizes a transfemoral approach to close off the left atrial appendage and reduce the risk of stroke. It has been, and continues to be the key growth driver of not just the Cardiovascular division, but also the entire BSX business. Management has recently upgraded their forecast for the LAAC market (in the abovementioned TCT update), now seeing $1.5bn in 2024, and $3bn in 2026, up from previous estimates of $1bn in 2023 and $2bn in 2025. Management looks to continue to grow this by increasing awareness of the product, and expand indication through CHAMPION-AF and OPTION trials (these indications are currently not included in the market estimates).

The near-term growth driver here is the Watchman FLX, the next generation device that comes in more size options and can treat a wider range of patients. I was also pleasantly surprised by Watchman’s double-digit growth in 3Q 2020, given the increasing hospitalization rates in the US, and also the more elective nature of Watchman procedures.

After having the playing field all to themselves for a few years, there is finally a competitor in sight (Abbott). Even though a new competitor is usually a bad thing, I have seen various cases, such as in the TAVR category, that a new competitor actually accelerates the growth of the addressable market, mainly due to increased awareness. As this is still a new-ish market, I believe that there is still a long runway and the product will continue to provide strong growth in the medium to long term.

Single-use scopes

BSX has had a good recent track record in its single-use scopes platform, successfully scaling LithoVue single-use ureteroscope and SpyGlass choliangoscope over the last few years. The company views this platform as a multi-billion market, as the market shifts from durable/reusable scopes to single-use scopes, mainly due to the difficulty in reprocessing/cleaning scopes, which leads to higher infection risk.

The key near-term opportunity here is EXALT D, a single-use duodenoscope. A duodenoscope is a camera attached to a tube that enters a patient’s small intestine, to allow the doctor to see and diagnose, in a procedure known as Endoscopic Retrograde Cholangiopancreatography (“ERCP”). Today there are around 1.5MM ERCP procedures performed annually around the world.

In the US, the FDA has been particularly concerned about durable duodenoscope infection. Duodenoscopes are difficult to clean, and the FDA has highlighted that 5.4% of reused duodenoscopes test positive for high concern organisms from previous ERCPs. Notably, the FDA issued a Safety Communication in 2019 advising hospitals and endoscopy facilities to transition to duodenoscope that facilitate or eliminate the need for reprocessing.

“It is unacceptable that 1 in 20 patients who undergo a procedure using a duodenoscope may acqure an infection”

Excerpt from Senator Patty Murray letter to scope manufacturers, May 2019

To be clear, EXALT D at around $2,500 per procedure is most likely more expensive than the amortized costs per surgery of a durable duodenoscope. However, given the increasing scrutiny by the FDA, and also the potential costs and trouble associated with a post-surgery infection, I believe that the shift to single-use will accelerate in the next couple of years, and will be a key growth driver for BSX in the medium term.

In addition to EXALT D, BSX has also been developing a comprehensive single-use portfolio, designed to reduce infection, enhance efficiency, and improve availability. Key products include SpyGlass DS II (cholangioscope), SpyGlass Discover (choledochoscope), EXALT B (bronchoscope), and EXALT TG (therapeutic gastroscope). Altogether this should be a $2bn market by 2024, with BSX a key player.

Management and acquisitions

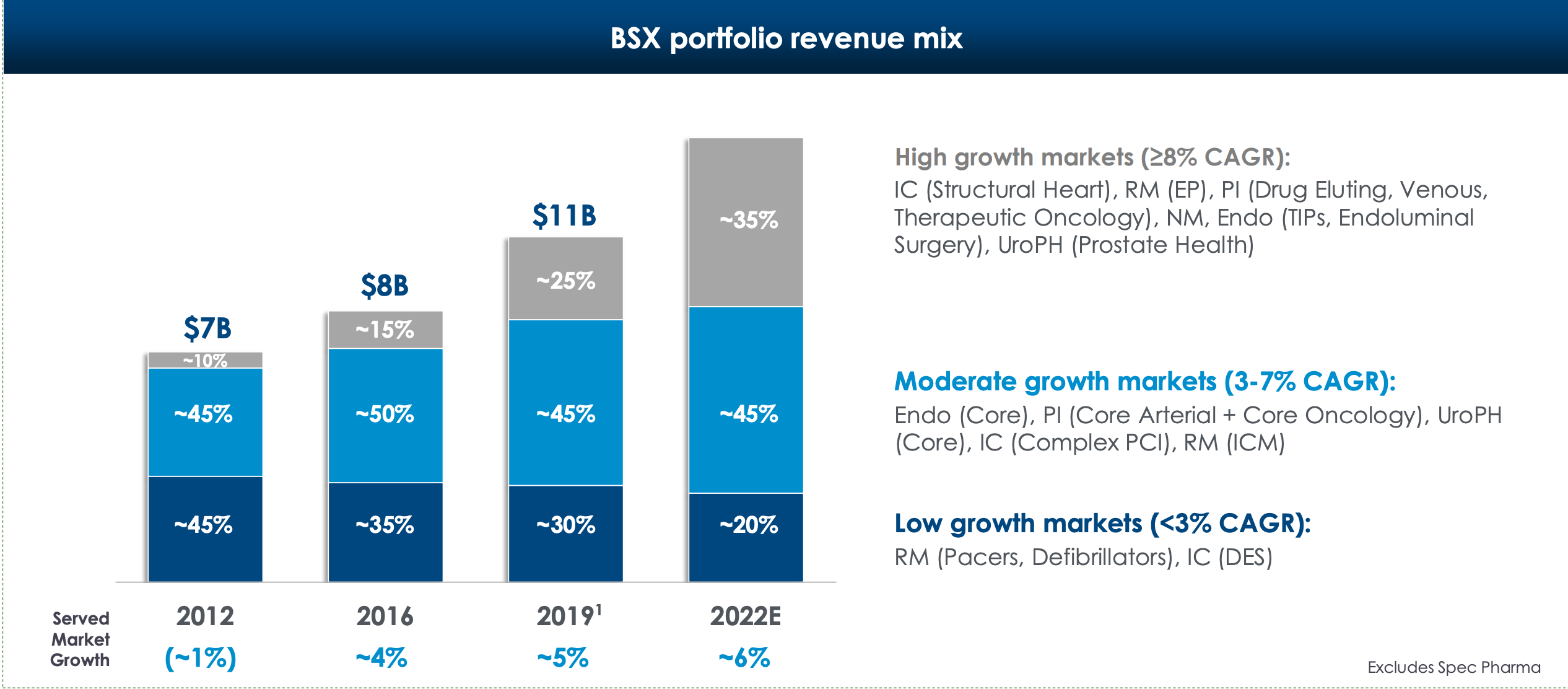

BSX has one of the most well-regarded management team in the Medical Devices industry, led by Michael Mahoney. Since he took over the helm around 2012, Michael has led a shift in the portfolio from lower-growth end markets to higher growth end markets, through internal R&D (R&D as % of sales is at the high-end of its peers), Venture Capital investments, and also strategic tuck-in acquisitions. Given the size of the existing portfolio, this has not been an easy task, but you can see signs of this shift across the entire portfolio in the different categories.

Source: Investor presentation by Boston Scientific Corp

BSX has over the last few years also focused on expanding outside of the US, especially in emerging markets. Continued expansion into Emerging Markets is one of the key growth drivers in the medium term, and the company expects to grow 15+% CAGR in Emerging Markets over the next few years. As of year-end 2019, 57% of revenues come from the US, and 43% is derived from Outside-US.

Acquisitions

Given the importance of acquisitions as a strategy to grow, I thought it would be important to have a quick overview of some of the company’s recent acquisitions, which were mostly tuck-ins, except for BTG.

BTG, which has just recently become organic to growth, was a $3.7bn acquisition net of cash. BSX has subsequently sold off the Pharmaceutical Licensing royalties and the Specialty Pharmaceuticals businesses for more than $1bn, leaving the core Interventional Medicines division, which was subsumed under Peripheral Interventions.

I like this acquisition as it gives BSX exposure to a strong vascular and interventional oncology portfolio, including TheraSphere Y90, which provides localized radiation delivery mainly for liver cancer. Furthermore, BTG had 90% of revenue coming from the US, and BSX can help to scale its products and technologies across the world through its global footprint, especially in Asia-Pacific. Management expects $175mm of cost synergies by Aug 2022, and to realize 80% of the synergies by Aug 2021. BSX is also utilizing this acquisition to expand into high-growth adjacencies such as Pulmonary Embolism and Cancer Therapies.

So far, the BTG acquisition seems to be playing out well for BSX. The company paid $2.7bn (net of cash and sale of the other two businesses) for a $400mm Interventional Medicines asset growing at low to mid-teens, with accretion to earnings and growth in 2021, and at the same time giving the company exposure to key growth markets at scale.

Other than BTG, BSX’s recent acquisitions have also been quite successful viewed in totality. A few key examples include Augmenix and its SpaceOAR asset, Vertiflex and its LSS asset, Claret and its Sentinel asset.

I have confidence this management has not only the ability to identify valuable assets at reasonable prices, but also have the ability to integrate acquired businesses, achieve cost synergies, and scale the acquired products and technologies quickly to other geographies and adjacencies.

Financials, numbers, and free cash flow

With the common stock trading at $33.14 (as of 30th Nov 2020), and around 1,431.92mm shares outstanding, market capitalization is ~$47.4bn, and enterprise value (“EV”) ~$55bn.

Capital stack

BSX’s capital stack includes $7.5bn of net debt, and common shares and convertible preferred shares issued in May 2020. BSX raised approximately $1.95bn in May this year through a 29.4mm common stock sale at $34.25 per share ($975mm), and 10.1mm 5.5% convertible preferred stock issue ($975mm), which will be automatically converted to common stock on 1 June 2023 with a conversion price of $41.96. At maturity, if the share price is less than $34.25, BSX will issue 28.47mm shares, if the share price is between $34.25 to $41.96, BSX will issue between 23.24mm shares to 28.47mm shares. If the share price is more than $41.96, BSX will issue 23.24mm shares.

This slightly complicates the math as the dilution is based on the share price, and will be more diluted as the share price falls, and less diluted as the share price rises. In general, such a structure serves to exacerbate price movements both upwards and downwards, unless the share price moves far away from the $34.25-$41.96 range. However, the difference in dilution is not significant in the long term, and will be adequately built into my margin of safety.

This is approximately a 4% dilution, and $750mm will be used to repay debt, and around $1.2bn will likely be used to deploy opportunistically in tuck-in investments. In retrospect, the management was probably expecting an extended period of low or even distressed asset prices due to COVID-19, and did not foresee such a sharp bounce back in asset values. Nevertheless, it was still a prudent move back in May, to shore up its balance sheet and accumulate dry powder for investing.

Gross debt to EBITDA is at 3.7x as of Sep 2020, and management is targeting 2.5x by year end 2021, with a long term goal of 2.25x. Note that due to the capital raise in May 2020, BSX has quite a bit of cash on hand, and at the same time generating strong free cash flow ($870mm in 3Q2020), so net debt to EBITDA is significantly lower than its gross debt to EBITDA.

The balance sheet looks healthier than ever, and stands the company in good stead to opportunistically deploy capital

Valuation

Earnings before Interest and Taxes (EBIT) for 2019 was around $2.8bn. BSX is trading at an EV/2019 EBIT multiple of 19.6x. Management is guiding for 6-8% top-line growth and 50-100bps Operating Profits Margin (“OPM”) expansion in the medium term, driving double digits Earnings Per Share (“EPS”) growth. Management has had a good track record in terms of guidance and executing against the guidance. From 2014-2019, BSX has grown organic revenue at a CAGR of around 6.5%, expanded OPM by 6%, and adjusted EPS at a CAGR of 14%.

In 2018 and 2019, BSX was growing topline organically at 7+%. Given that the TAVR setbacks mentioned above (Lotus and Acurate) were small businesses back then, Watchman was just starting to grow, and that there were a few unexpected notable setbacks in 2019 (Paclitaxel and Spinal Cord Stimulation), its medium-term outlook of +6-8% seems achievable.

Assuming OPM expansion to 29% in 2023 (around 80bps per year), EBIT should grow at around 10% CAGR from 2019-2023 to $4.07bn. At a 1 year forward EV/2023E EBIT multiple of 20x, year-end 2022 EV would be at around $81bn. Assuming net debt of $11bn then, and that number of shares outstanding stay constant, the share price will be higher by approximately 48%, which is a good return (for me) for a 2-years holding period.

Another reason why I am bullish is that for the first time in a few years, the company will have access to the free cash flow (“FCF”) generated. For the last few years, there have been various claims to the cash, such as litigation settlements and a tax dispute with IRS. As earnings translate into FCF, BSX should have access to a substantial amount of cash within these few years to opportunistically deploy into reinvestments, tuck-in acquisitions, or share repurchases (even though it might seem weird as they recently sold shares. However, if the share price falls further, I wouldn’t be surprised if management tactically buys back shares at a lower price at which they sold, if there are no other attractive investment options).

Key risks

1) Continued slowdown from CRM and Coronary Stents businesses, which are both large businesses for BSX. Coronary Stents is one of the most mature markets in the Medical Devices industry, and has been under significant pricing pressures over recent years, with limited innovation. On a value basis, the market has been at most flat, if not down despite steady volume growth. That said, BSX has been a leader in Coronary Stents for the longest time, and it is still a significant part of BSX’s business despite being dilutive to the company’s growth profile.

CRM’s high and low voltage businesses have also been slowing for BSX, with higher growth in Insertable Cardiac Monitor and Electrophysiology (technically not under CRM, but often lumped together).

Management seems to be well aware of this risk, and has been proactively managing the portfolio. As a result, CRM and Coronary Stents have become a much lower percentage of the business as compared to a few years ago.

2) COVID-19 taking longer than expected. BSX has a higher exposure to less acute/more elective procedures. With the recent spike in hospitalization cases in the US and Europe, some of the procedures might get delayed, or canceled. On the bright side, hospitals are better able to adapt to this recent spike as compared to March/April 2020, so many of the procedures are still ongoing. Also, management has shown the ability to cut costs quickly, and some of the savings will likely be more permanent, such as more video calls and less traveling

3) Another negative surprise in one of its key products in the near term. I understand that discontinuing failed products and facing setbacks in clinical trials are part and parcel of this industry, but if there is another negative surprise in one of BSX’s key products in the near term, investors will really question the “premium portfolio, higher-growth than market” BSX story, and multiple will most likely de-rate together with forward estimates

P.S. I am just starting to write more frequently. If you have any feedback, click “reply” or comment below.

If you like what you are reading, please help to share this article with your friends or on Twitter.

Disclaimer: This is not investment advice. I am merely detailing and documenting my investment and thought process. Please do your own due diligence before investing.

I currently have a long position in Boston Scientific Corp shares.